Introduction

Singapore's brand landscape is unusually shaped by its government-linked companies (GLCs). Household names like DBS, Singtel, PSA International, and Singapore Airlines consistently rank among the nation's most valuable brands, yet they operate under fundamentally different branding constraints than their private sector peers.

The top three Singapore-listed state-owned enterprises alone accounted for 26.1% of Singapore Exchange (SGX) market capitalisation as of April 2024. That concentration reflects something deeper: ownership structure shapes how a brand is built, managed, and perceived.

The answer lies in understanding the unique position GLCs occupy. Unlike fully government entities that rely on mandated engagement, GLCs compete commercially in open markets — domestically and internationally. Yet they carry a public trust dimension that private companies don't. Their brands are partly seen as extensions of Singapore Inc.

This article explores the key dimensions where GLC and private sector branding diverge: purpose and mandate, stakeholder structure, visual identity norms, decision-making speed, and the growing convergence between the two sectors.

TLDR

- GLCs must balance national interest with commercial competitiveness — this tension shapes every branding decision they make

- Private sector brands enjoy more creative freedom and faster decision cycles

- GLC branding involves more stakeholders and longer timelines

- Both sectors are converging, with GLCs increasingly adopting commercially sophisticated strategies

- The right branding partner knows which constraints are fixed and which boundaries can be challenged

What Are GLCs in Singapore and Why Does Branding Matter for Them?

In the Singapore context, GLCs are companies where Temasek Holdings or the government holds a significant equity stake. Singapore's GLC density is notably high relative to other developed economies — according to the OECD, state-owned enterprises in markets like Singapore, China, Malaysia, and Vietnam account for over a third of market capitalisation.

Key examples include:

- DBS (28% Temasek stake) — largest Singapore bank by market cap

- Singtel (51% Temasek stake) — majority-owned telecommunications provider

- Singapore Airlines (53% Temasek stake) — national carrier

- PSA International (100% Temasek stake) — wholly-owned global port operator

- CapitaLand Group (100% Temasek stake) — privatised real estate group

- Keppel Ltd (20% Temasek stake) — diversified conglomerate

- Sembcorp Industries (50% Temasek stake) — energy and urban development

As at 31 March 2025, Temasek's net portfolio value stood at S$434 billion, with 52% of the portfolio consisting of companies headquartered in Singapore.

Why Branding Matters for GLCs

Unlike pure public sector bodies such as ministries or statutory boards, GLCs must compete commercially for customers, revenue, and market share. They cannot rely on mandated engagement. This means they must build brand equity to win in the marketplace.

Yet GLCs carry a constraint private companies don't: public accountability. Their brands are scrutinised not just for commercial performance, but for alignment with national strategic interests. A DBS outage isn't merely a service disruption — it becomes a regulatory matter. When the Monetary Authority of Singapore (MAS) imposed a six-month pause on DBS's non-essential IT changes in 2023 following repeated digital service disruptions, CEO Piyush Gupta's variable compensation was cut by 30% (approximately S$4.1 million). No private sector brand faces that kind of institutional consequence.

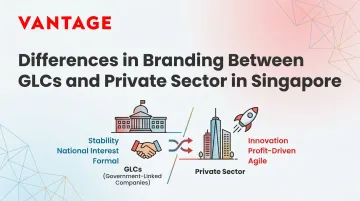

Brand Purpose and Mandate: National Interest vs. Commercial Drive

GLCs operate under a dual mandate: they must simultaneously serve national strategic interests AND compete commercially. This fundamentally shapes their brand purpose.

The Dual Mandate in Action

Consider Singapore Airlines. SIA's brand must project national pride and aspiration while competing fiercely against Gulf carriers and low-cost rivals. The airline's "Welcome to World Class" global brand campaign (launched January 2023) was filmed across Singapore, Auckland, Barcelona, Mumbai, and Shanghai — positioning SIA as a global premium carrier while anchoring its identity in Singapore's national brand.

In the 2026 Brand Finance Singapore 100 report, Singapore Airlines ranked 1st among Singaporean respondents for sustainability perception efforts, with its commitment to net-zero carbon emissions by 2050 framed as both a commercial differentiator and a national ESG leadership signal.

DBS provides another clear example. The bank's "Live more, Bank less" brand promise positions banking as an enabler of better lives, not an obstacle. But this commercial messaging is consistently paired with public-interest initiatives. DBS launched a S$1 billion, 10-year community impact programme in 2024 to support vulnerable communities, and partnered with IMDA (Infocomm Media Development Authority) to target approximately 100,000 beneficiaries for digital inclusion over 2023-2024.

When DBS created the TableTok campaign, it explicitly framed financial literacy as a public responsibility — responding to research showing 55.2% of surveyed Singaporeans considered themselves financially illiterate. This wasn't just a marketing play; it was brand purpose anchored in national good.

Contrast with Private Sector Brand Purpose

That kind of dual accountability doesn't exist in the private sector. Commercial brands like Circles.Life or Grab build their entire identity around disruption, speed, or irreverence — with no obligation to national optics. Their brand purpose is defined by founders and investors, not public mandates.

Circles.Life — a digital telco challenger launched in 2016 — deliberately courts controversy to generate buzz. As its Senior Regional Manager for Brands and Campaigns stated at the Marketing Interactive Content 360 conference: "You have to be controversial, you have to have people who hate it...unless you have polar opposite conversations, nobody is going to talk about your campaign."

The brand executed stunts including:

- "Vandalism" of a fake competitor ad at an MRT station (March 2017)

- A cash-dispensing vending machine at Raffles Place that drew nearly a thousand people and required police intervention (February 2018)

- An open letter to Singtel and StarHub accusing them of product mimicry

This approach delivered a +50 Net Promoter Score and captured over 5% market share. But it's a strategy no GLC brand could pursue without risking parliamentary questions or media scrutiny framed around public accountability.

How the Dual Mandate Shapes Messaging and Risk Tolerance

GLC brands anchor their purpose in broader societal or national narratives. Their messaging must appeal across Singapore's diverse population and avoid choices — visual or verbal — that could generate political controversy.

Private sector brands can court controversy to generate buzz. GLCs almost never can. The downside for a GLC isn't just commercial backlash — it's regulatory scrutiny, political commentary, and damage to institutional credibility.

This raises a genuine strategic challenge: because GLC purpose is partly externally mandated, the brand must work harder to feel earned rather than assigned. The most effective GLC brands — SIA and DBS among them — succeed when they make national interest feel like a natural extension of customer value, not a compliance checkbox.

Stakeholder Complexity and Brand Governance

The Stakeholder Landscape

For a typical GLC rebrand, the stakeholder landscape includes:

- Ministry of Finance or relevant line ministry

- Temasek Holdings as shareholder

- GLC board of directors

- C-suite leadership

- Business unit heads

- Unions (in some cases)

- General public (who perceive the brand as quasi-public property)

Contrast this with a private sector rebrand, which typically involves:

- Founders or PE/VC investors

- CEO

- Small leadership team

That gap in stakeholder complexity directly affects timelines, process, and how much creative ambition the project can sustain.

How Stakeholder Complexity Affects Timelines

GLC branding projects typically involve multiple rounds of approvals at different organisational levels, formal governance committees, and sometimes public or ministerial sign-off.

Industry benchmarks suggest a strategic brand review — covering research, message development, and design — typically takes 12–14 weeks for a commercial client, with a further 2–3 months for campaign rollout. GLC projects of comparable scope routinely run longer. Procurement processing, internal approval rounds, and governance requirements each add time that private sector clients simply don't face.

Six factors consistently extend timelines:

- Branded asset inventory and lead times

- Operational cycles

- Internal review and approval processes

- Resource allocation

- Legal and regulatory requirements

- Business drivers and budget interdependencies

For GLCs, factors 3, 5, and 6 create the most friction.

The Procurement Dimension

Many GLCs are required to go through formal government procurement or open tender processes when engaging branding agencies. Singapore government procurement operates through GeBIZ, the centralised procurement platform, with structured thresholds:

| Procurement Category | Estimated Value | Method |

|---|---|---|

| Small Value Purchases | Up to S$6,000 | Verbal or written quotes |

| Quotation | Up to S$90,000 | Open or Limited Quotation via GeBIZ |

| Tender | Above S$90,000 | Open, Selective, or Limited Tender via GeBIZ |

| Tender Lite | Up to S$1,000,000 | Simplified tender conditions, no security deposits |

While GLCs are not strictly bound by GeBIZ rules (which apply to government agencies), many adopt comparable governance standards due to their ownership structure and public accountability expectations.

In practice, agency selection involves evaluation rubrics, shortlisting committees, and compliance documentation. A private sector company can select and brief a branding agency within days. For a GLC, the same decision typically takes weeks — sometimes months.

Internal Brand Governance

GLC internal brand governance tends to be more formalised:

- Brand standards committees overseeing visual and messaging consistency

- Mandatory adherence to group-level visual identity systems (especially for Temasek-linked entities)

- Internal approval chains for any public-facing brand material

Private sector companies — especially SMEs and startups — often operate with informal brand governance, relying on a single brand champion.

Navigating this environment effectively requires a branding partner who can operate within structured governance frameworks without letting process crowd out strategy. Vantage Branding has worked with organisations including PSA, MPA, Enterprise Singapore, and Sentosa — each with their own approval structures and stakeholder layers — and understands how to keep the creative work sharp while the governance process runs its course.

Brand Voice, Visual Identity, and Creative Expression

Visual Identity Conventions

GLCs frequently incorporate national colours, formal typography, and measured visual systems that project stability, trustworthiness, and institutional longevity. These conventions signal credibility and permanence — essential for organisations stewarding national infrastructure, financial systems, or strategic assets.

Private sector brands — especially in tech, F&B, and consumer retail — are far more likely to use bold, irreverent, or culturally specific visual languages to stand out and attract younger audiences.

Brand Voice Divergence

GLC brand voice tends to be:

- Considered and inclusive

- Authoritative without being authoritarian

- Avoiding slang, extreme personality, or polarising positions

Private brands can build their entire identity around a strong, even niche, voice. A fintech brand might talk like a savvy millennial. A food brand might adopt a cheeky hawker persona. These voices would be unworkable for a GLC.

The Creative Risk Appetite Gap

Private sector brands can take bigger visual and narrative risks because the downside is limited to commercial performance. For GLCs, a misaligned brand campaign can generate public criticism, political commentary, or damage to institutional credibility.

This shows up in how creative briefs are written and how agencies are expected to respond. GLC briefs tend to be more tightly defined, with tighter guardrails around tone, messaging, and visual direction.

The Growing Exception

Some GLCs have deliberately pushed their visual and verbal identity further in recent years to remain competitive and attract talent. DBS is the clearest example of how far that shift can go.

DBS evolved its strategic narrative over 15 years — moving from a "house" metaphor under former CEO Piyush Gupta to a "lighthouse" metaphor under new CEO Tan Su Shan (2025): "In turbulent times, we want to be that lighthouse that people gravitate towards — a haven in a sea of volatility."

Key markers of that creative evolution include:

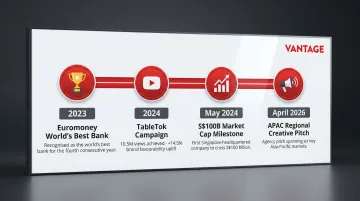

- Agency review (April 2026): DBS launched a creative pitch across six Asia-Pacific markets to find a regional partner — the largest known creative review by a Singapore GLC, anchored around protecting a US$18.6 billion brand value

- TableTok campaign (2024): Won Influencer Marketing Gold at The Drum Awards for Marketing APAC, with 10.5 million views and brand lift across favourability (+14.5%), consideration (+13%), and recommendation (+11%)

What this signals is less about creativity for its own sake and more about competitive necessity. As GLCs compete for talent, customers, and relevance alongside private sector players, the brand strategies that once set them apart now risk making them invisible.

Branding Process: Speed, Agility, and Decision-Making

The Speed Differential

A well-resourced private company can move from brand strategy brief to new identity launch in three to six months. A GLC project of similar scope often takes two to three times longer — procurement lead times, multiple internal approval rounds, and governance requirements all add up.

This speed difference affects creative output. GLC branding work tends to be more thoroughly researched and tested before launch — which has quality benefits — but can also result in work that feels slightly less culturally urgent or timely.

Private sector brands can react to cultural moments, respond to competitors, or iterate on identity in near real-time.

Implication for Agency Relationships

That speed gap shapes what each type of client actually needs from an agency. GLCs typically look for partners that are:

- Patient and process-disciplined

- Skilled at stakeholder management

- Experienced in navigating governance structures

- Able to maintain creative ambition within constraints

Private sector clients often prize:

- Speed and entrepreneurial energy

- Creative boldness

- Minimal process overhead

Agencies that work across both sectors develop a distinct muscle: they know when to slow down for rigour and when to move fast before the moment passes.

The Convergence Trend: When GLCs Brand Like Private Companies

There is a clear trend of Singapore GLCs investing in more sophisticated, commercially aggressive branding over the past decade.

Evidence of Convergence

DBS's digital banking transformation positioned the bank as the "World's Best Digital Bank," winning Euromoney's World's Best Bank award three years running (2023–2025) and becoming the first Singaporean company to cross S$100 billion in market capitalisation (May 2024).

Singtel's 5G brand campaigns and SIA's post-pandemic relaunch similarly show GLCs matching private sector levels of brand investment and creative ambition.

Singapore's top 100 brands are collectively valued at USD 84.1 billion in 2026, up 7% year-on-year, with GLCs dominating the rankings:

| Brand | Brand Value (2026) | Rank | Notes |

|---|---|---|---|

| DBS | USD 18.6 billion | #1 | 14th consecutive year as #1 |

| Singtel | USD 4.1 billion | #6 | — |

| Changi Airport | USD 889 million | — | #1 Strongest Brand (91.2 AAA+) |

DBS also ranked #1 on LinkedIn's Top Companies list in Singapore for both 2025 and 2026 — rated the best workplace for career growth. That result signals that strong employer branding has become as critical for GLCs as commercial brand-building.

Drivers of Convergence

GLCs now face genuine competitive pressure from faster-moving local competitors and global players. Attracting young talent means competing against private sector employers on brand appeal, not just job security. And as these companies expand internationally, they need brands that hold up on their own — without relying on a Singapore government backstory to do the heavy lifting.

This convergence has also been encouraged by Temasek's push for its portfolio companies to be globally competitive. Temasek states: "Guided by stewardship principles, we actively engage our Singapore-based Temasek Portfolio Companies to strengthen their resilience and position for long-term growth."

What Private Brands Can Learn

GLCs' long-term brand discipline — consistent messaging, sustained investment even during slow growth periods — offers a stability model that fast-scaling private brands often sacrifice in favour of short-term campaigns.

The strongest brand strategies borrow from both playbooks: GLC-style consistency paired with private sector creative agility. For organisations navigating that balance, working with a branding partner experienced across both sectors, like Vantage Branding, can help avoid the pitfalls of either extreme.

Frequently Asked Questions

What are the GLC companies in Singapore?

Key Singapore GLCs include DBS, Singtel, PSA International, Singapore Airlines, CapitaLand, Keppel, and Sembcorp Industries. These are companies where Temasek Holdings or the government holds a significant equity stake, and they collectively represent over a third of Singapore's stock market capitalisation.

What is the difference between public and private companies in Singapore?

Public companies, including GLCs, are linked to government ownership and operate with dual accountability — commercial performance and public interest. Private companies are owned by founders or investors and focus purely on commercial returns, without public accountability obligations.

Do GLCs in Singapore invest in branding the same way private companies do?

GLCs invest significantly in branding — DBS's US$18.6 billion brand value reflects that commitment — but the approach differs. Processes are more structured, timelines are longer, and a broader set of stakeholders is involved compared to private sector engagements.

Why do GLC brands in Singapore tend to look more conservative than private sector brands?

This reflects their dual accountability to commercial performance and public trust. GLC brands must appeal broadly across Singapore's diverse population and avoid visual or verbal choices that could generate political or public controversy. Conservative design signals stability and institutional credibility.

Can private branding agencies work with GLCs in Singapore?

Private branding agencies regularly work with GLCs, but must be prepared for government procurement processes, multi-stakeholder approvals, and stricter governance requirements. Agencies with public sector experience are better positioned to navigate these.

How is GLC branding changing in Singapore?

GLCs are increasingly adopting bold, commercially sophisticated brand strategies — driven by global competition, talent acquisition, and international expansion. DBS, SIA, and Singtel now invest in brand building at levels that match or exceed private sector benchmarks, while retaining the institutional credibility their heritage provides.