Introduction

Malaysia's fintech sector is booming. Digital banking licenses are active, DuitNow QR exceeds 3 million merchant touchpoints, and new players launch every quarter. Yet despite this growth, most users struggle to tell one fintech brand from another.

Features converge quickly — faster transfers, lower fees, better interfaces — but brand identity remains the one competitive advantage competitors cannot replicate.

Malaysian fintech founders and marketers face a distinct challenge: building brands that earn trust across a multicultural population, satisfy Bank Negara Malaysia's regulatory expectations, and still feel modern and approachable.

Generic global branding playbooks won't cut it here. Malaysia's ecosystem demands culturally intelligent, compliance-forward brand strategies built specifically for this market.

TLDR

- Malaysian fintech operates under BNM's digital banking framework—compliance signalling must be built into brand identity from day one

- Malaysia's multicultural society (Bumiputera 70.1%, Chinese 22.6%, Indian 6.6%) demands culturally intelligent brand decisions across color, language, and messaging

- Trust drives fintech adoption in Southeast Asia; brand identity is the primary vehicle for building it

- Consistent branding across apps, onboarding, and investor materials compounds credibility over time

- Look for branding partners with deep regional knowledge of Malaysia's market dynamics, not just design capability

Malaysia's Fintech Ecosystem: The Branding Opportunity

Malaysia's fintech sector generated approximately USD 485 million in revenue from digital investment and digital assets segments, according to Statista. This figure represents just a portion of the broader ecosystem, which includes digital wallets like Touch 'n Go eWallet and Boost, digital banks such as GXBank and AEON Bank, and national infrastructure like DuitNow QR, which now surpasses 3 million registered touchpoints.

Government Framework Raises the Credibility Bar

Bank Negara Malaysia issued five digital banking licenses on April 29, 2022, under the Policy Document on Licensing Framework for Digital Banks. All five—GXBank, Boost Bank, AEON Bank, Ryt Bank, and KAF Digital Bank—have commenced operations as of December 2024.

Malaysia's MyDIGITAL blueprint targets the digital economy to contribute 22.6% of GDP by 2025, with goals that include:

- 5,000 new startups

- RM70 billion in digitalization investment

- 875,000 MSMEs adopting eCommerce

This structured, regulated environment creates a high brand credibility bar. Licensed players must look and feel trustworthy by design—not just compliant on paper, but visually, verbally, and experientially credible across every customer touchpoint.

The Inflection Point for Brand Investment

Early fintech differentiation focused on features: faster transfers, lower fees, better UX. As the market matures, feature parity is no longer a differentiator. Brand loyalty and trust perception now drive switching decisions more than marginal product improvements. That shift is precisely where brand identity investment delivers its highest returns—before the market becomes too crowded and customer acquisition costs spiral.

Why Brand Identity Is Mission-Critical for Malaysian Fintechs

Trust Remains the Primary Adoption Barrier

Research confirms that trust is a significant factor influencing Malaysians' intention to accept digital banks, alongside compatibility and perceived benefit. The EY Global FinTech Adoption Index 2019 found that 22% of fintech non-adopters globally cited greater trust in incumbents over fintech challengers as a primary barrier.

Brand identity is the primary signal of legitimacy before a user opens an account. A polished, coherent visual system and clear messaging about security and data privacy tell prospective customers this company is serious, stable, and safe—far more immediately than any features list.

Brand Consistency Reduces Customer Acquisition Costs

When a brand is recognized and trusted, paid marketing converts better, word-of-mouth activates more readily, and onboarding friction decreases. Malaysian fintech customer acquisition is expensive in a multi-player market where digital wallets, digital banks, and payment platforms compete for the same users. A strong brand identity lowers the cost of every conversion by reducing the persuasion burden on paid channels.

Regulatory Credibility Through Professional Branding

In BNM's regulated environment, brand presentation is itself a credibility signal. Regulators and enterprise partners read visual consistency as evidence of operational discipline. Startups with inconsistent fonts, generic stock imagery, and unclear value propositions raise an unspoken question: if they can't define their own identity, can they be trusted to manage someone else's money?

Attracting Investors and Enterprise Partners

Strong brand identity communicates organizational maturity and strategic clarity. Tracxn data shows 163 Malaysian fintechs have received funding, totaling approximately USD 707 million cumulatively. However, funding dropped sharply from USD 257 million in 2022 to USD 7.7 million in 2024 before rebounding to USD 33.6 million in 2025.

In a tighter investment climate, investors apply sharper scrutiny. A coherent brand signals readiness across three dimensions:

- Positioning clarity — the team knows who they're for and why they win

- Execution discipline — consistent identity reflects operational rigor

- Market confidence — a polished presence suggests the company is built to last

Differentiation in a Multi-Product Market

Users in Malaysia often use multiple fintech products simultaneously—one for savings, another for payments, a third for remittances. Strong brand identity is what determines which app users open first. When products are functionally similar, the one with a clearer, more trusted identity captures the primary relationship—and holds it.

Malaysia's Unique Branding Landscape: Culture, Compliance, and Community

Multicultural Branding Is Not Optional

Malaysia's citizen population comprises Bumiputera (70.1%), Chinese (22.6%), and Indian (6.6%). Each community carries distinct cultural values, language preferences, and visual associations. Color choices, imagery, and language code-switching must be deliberate brand decisions.

Color symbolism varies sharply:

| Color | Malay Cultural Meaning | Chinese Cultural Meaning |

|---|---|---|

| Red | Bravery, medicinal significance | Joy, celebration, good fortune |

| Yellow/Gold | Royalty, sovereignty | Wealth, prestige, authority |

| Green | Freshness, youth | Growth, health—but "green hat" implies infidelity |

| White | Purity, cleanliness | Mourning, death—avoid for celebrations |

| Black | Varies by shade | Power, formality—but can imply "shady" dealings |

Fintech brands that feel culturally generic often feel culturally exclusionary. Yellow/gold emerges as the safest cross-cultural premium signal: royalty in Malay culture, wealth in Chinese culture.

Islamic Finance as a Competitive Differentiator

Malaysia's Islamic banking assets surpassed USD 260 billion by end-2024, accounting for 43% of domestic system loans. AEON Bank operates as Malaysia's first digital Islamic bank, positioning itself around ethical banking, Shariah compliance, and financial inclusion.

A significant portion of the population expects fintech products to signal Shariah alignment where relevant. Shariah-compliant positioning opens access to Malaysia's largest consumer segment while signalling ethical values that resonate across communities.

The "Caregiver" Brand Archetype Resonates

Malaysia's fintech ecosystem responds strongly to brands positioned around inclusion, community uplift, and accessible empowerment. DuitNow QR's story—3 million touchpoints with 267,780 new MSME acceptance points added in 2025 alone—exemplifies this archetype. Brands positioned as enablers, not extractors, build deeper emotional connections.

Practically, this means:

- Brand voice that emphasises partnership, not transactions

- Imagery featuring real Malaysian communities, not stock photos

- Storytelling that highlights customer success, not product features

- Messaging that positions financial services as tools for empowerment, not status

Nation-Building Narrative Opportunity

Malaysian fintech brands can authentically position themselves as contributors to the country's digital economy ambitions. Brands aligned with financial inclusion, empowering the underserved, or building Malaysian economic resilience tap into a story that resonates with consumers, regulators, and the press simultaneously.

Brands aligned with these government priorities — MyDIGITAL's 22.6% GDP target and 875,000 MSMEs adopting eCommerce — earn credibility with consumers, regulators, and press alike. That alignment belongs at the centre of brand positioning, not confined to a CSR page.

Compliance Communication as a Brand Pillar

BNM's framework requires transparency about data usage, security practices, and financial protections. Fintech brands must design identity systems that include these trust signals naturally—not as footnote disclaimers, but as front-and-center brand commitments.

This is achieved through:

- Tone of voice that balances authority with accessibility

- Iconography that visually communicates security and transparency

- Onboarding copy that explains protections without legal jargon

- Visual hierarchy that prioritises trust signals in user flows

Core Elements of a Fintech Brand Identity in Malaysia

Brand Positioning and Value Proposition

Clear positioning is the foundation. It defines who the brand serves, what problem it solves, and why it differs from alternatives—including traditional banks. In Malaysia's market, positioning must account for the specific segment: gig workers, SMEs, underbanked communities, Muslim consumers, or digital-native millennials. Vague positioning produces vague brands.

Visual Identity System for a Mobile-First Market

94.4% of Malaysian internet users access the internet via smartphone, according to MCMC. Smartphone penetration reached approximately 89.29% of the total population in 2024.

Visual identity must perform at small scales:

- Logo design: Scalable and recognizable at app icon scale

- Color palette: Account for cultural color associations across Malaysia's multicultural context (yellow/gold as safe premium signal; avoid white for celebratory contexts)

- Typography: Works across Bahasa Malaysia and English, readable at mobile sizes

- Dark/light mode compatibility: Essential for modern fintech apps

Brand Voice and Multilingual Messaging

Malaysian fintech brands need a defined tone of voice—typically balancing financial authority with everyday accessibility. The language landscape is complex:

- Bahasa Malaysia as the national language

- English as the business language

- Widespread Malay-English code-switching (Manglish) in digital communications

Academic research confirms that code-switching carries significantly less stigma in Malaysia than in Western markets and is the norm among bilingual speakers.

Brand guidelines must address how tone and register shift across channels—formal in investor materials, conversational in social media—without losing core personality. Getting this right is not a nice-to-have; it determines whether the brand feels native to its audience or imported.

Brand Story and Purpose

Every successful fintech brand needs a clear narrative: why does this company exist, who is it fighting for, and what does a better financial future look like?

Storytelling anchored in financial inclusion, community resilience, or economic empowerment builds stronger audience connection than feature-led communication—particularly with segments the traditional banking system has historically underserved. This also aligns with BNM's stated mandate for digital banks: serve the unserved and underserved, not just the already-banked.

Brands that communicate why they exist earn trust faster than those that lead with product specs.

Brand Consistency Across All Touchpoints

Critical touchpoints for Malaysian fintech brands:

- App UI and onboarding screens

- Website

- Social media (TikTok leads with 30.7 million users, followed by YouTube and Facebook)

- WhatsApp (90.7% monthly usage among internet users)

- Customer support interactions

- Agent/merchant-facing materials

- Investor decks

Inconsistency across these touchpoints is the fastest way to erode trust—especially when users move between an app, a WhatsApp interaction, and a social media ad in the same session. A brand system—design system + voice guide + messaging architecture—keeps all of it coherent without requiring case-by-case decisions at every channel.

Practical Strategies for Building Your Fintech Brand Identity

Ground the Brand in Audience Research

Start with qualitative and quantitative research into the specific Malaysian user segment being served—their financial behaviors, trust triggers, cultural reference points, and digital habits. Brands built on assumptions rather than insight fail to resonate across Malaysia's diverse consumer base.

A useful research brief should cover:

- Payment behaviors and preferred channels (e.g., QR, e-wallet, bank transfer)

- Trust triggers specific to each demographic (Chinese, Malay, Indian communities)

- Digital habits and platform usage (TikTok, WhatsApp, Shopee)

- Language preferences across touchpoints

Design for Mobile-First and QR-Native Experiences

Malaysia has 35.4 million internet users (98% penetration) and 44 million mobile connections (122% of population). DuitNow QR processed 8.44 billion digital payment transactions in 2025, with cross-border QR transactions reaching 29.7 million.

Brand identity must be tested and optimized for the contexts where users actually encounter it:

- Small app icons

- QR code landing pages

- Push notification copy

- In-app messaging flows

- Social media content (especially TikTok and Instagram Stories)

Your brand will live on a 6-inch screen first, a desktop second. That means logos must hold at 32×32px, color contrast must pass accessibility checks on OLED displays, and copy must land in under three seconds.

Build Cultural Flexibility Without Sacrificing Coherence

Create a core brand architecture that remains consistent—positioning, logo, primary color palette—while allowing for culturally adapted execution in campaigns:

- Different language versions (Bahasa Malaysia, English, code-switched Manglish)

- Culturally relevant imagery that reflects Malaysia's diversity

- Festival-specific visual treatments (Hari Raya, Chinese New Year, Deepavali) that feel authentic without breaking the brand system

The goal is a brand system flexible enough to feel local in every context, without requiring a redesign each time the calendar changes.

What to Look for in a Fintech Branding Partner in Malaysia

Regional Market and Cultural Intelligence

The most important quality is demonstrated understanding of Malaysia's multicultural landscape, Islamic finance considerations, BNM regulatory context, and competitive fintech dynamics. Generic global agencies tend to apply frameworks that miss local context entirely.

Look for case studies, cultural insight, and regional team members who understand the local market. Agencies like Vantage Branding, a Singapore-based agency with cross-border experience across Singapore and Malaysia, bring this perspective to technology and B2B engagements.

Their work with regulated industries, including financial services clients like Heritas Capital Management and Golden Equator Group, demonstrates the ability to navigate compliance requirements while building compliant, distinctive brand identities.

Full-Service Brand Strategy Capability

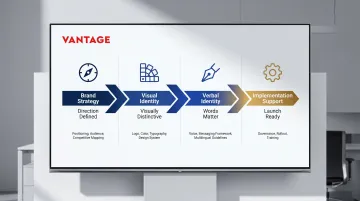

A fintech brand identity requires:

- Brand strategy: Positioning, audience definition, competitive mapping

- Visual identity: Logo, color, typography, design system

- Verbal identity: Voice, messaging framework, multilingual guidelines

- Implementation support: Brand governance, rollout planning, training

Ask prospective partners to show their full process and portfolio evidence across all these dimensions, not just visual deliverables. Visual work without strategic grounding looks good but rarely moves the needle on positioning or growth.

Collaborative Process and Ongoing Support

The best brand outcomes come from agencies that challenge assumptions, ask hard questions, and treat the engagement as a partnership rather than a production job.

Ask agencies about:

- Discovery phase rigor—how do they gather insights?

- How they handle revision cycles and client feedback

- Whether they provide launch support and brand governance guidance post-delivery

- Examples of how they've pushed back on client briefs to deliver stronger outcomes

The right partner will push back, ask uncomfortable questions, and stay invested in the outcome well past the final delivery.

Frequently Asked Questions

Is fintech legal in Malaysia?

Yes, fintech is legal and actively regulated in Malaysia under Bank Negara Malaysia's frameworks, including the Financial Services Act 2013, Islamic Financial Services Act 2013, and the Policy Document on Licensing Framework for Digital Banks. Licensed digital banks and e-money operators operate under formal BNM approval.

Is fintech in demand in Malaysia?

Yes — and the numbers show it. DuitNow QR surpassed 3 million merchant touchpoints, and PayNet processed 8.44 billion digital payment transactions in 2025. Government-backed initiatives like the MyDIGITAL blueprint (targeting 22.6% GDP contribution) continue driving fintech adoption across both urban and rural Malaysia.

How big is the fintech market in Malaysia?

Statista estimates Malaysia's fintech sector generated approximately USD 485 million in revenue from digital investment and digital assets segments. Non-bank transaction volume grew 71.7% year-on-year, reflecting the rapid expansion of the digital payments ecosystem.

Who are fintech companies in Malaysia?

Key players include digital wallets (Touch 'n Go eWallet, Boost), digital banks (GXBank, AEON Bank, Boost Bank, Ryt Bank, KAF Digital Bank), remittance and payments platforms (BigPay, Merchantrade, MoneyMatch), and international players with Malaysian operations (Wise, 2C2P, Mastercard).

What makes fintech brand identity in Malaysia different from other markets?

Several factors set Malaysia apart: a multicultural consumer base demanding culturally intelligent branding, Islamic finance accounting for 43% of domestic system loans, BNM's compliance-forward regulatory environment, and a national financial inclusion agenda. Together, these shape brand strategy decisions that generic global frameworks simply don't address.

How do I build trust through fintech branding in Malaysia?

Establish a consistent visual and verbal identity that signals professionalism, communicate security and compliance commitments as brand values (not fine print), align with a purpose that resonates culturally (financial inclusion, community empowerment), and maintain consistency across every user touchpoint — from the app to customer service.